Navigating Finance

Published by Don Hannay in Finance · Wednesday 04 Oct 2023

Tags: Navigating, Finance, finance, money, budgeting, investing, financial, planning, saving, personal, finance, financial, goals

Tags: Navigating, Finance, finance, money, budgeting, investing, financial, planning, saving, personal, finance, financial, goals

Navigating Finance

Lending for property in Australia still presents a number of obstacles for first home buyers. A key element of this is that borrowers are constrained by

- what they can buy

- where they can buy

- how much banks will lend

- hefty in-going costs such as stamp duty (albeit some concessions)

- increasing costs of housing

As a consequence, so are their opportunities, choices and lending options.

You don't need to be a mechanic to drive a car

There are over 90 financial institutions in Australia

An answer to this information and product congestion is to use a mortgage broker. A mortgage broker is a lending specialist and acts as an intermediary between you and a lender. Collectively mortgage brokers introduced about 70% of approved residential loans in Australia in 2023. So the service they offer is popular and it's a growing trend.

Consumer feedback suggests people like using a mortgage broker because

- it's less of a hassle than doing it yourself. That can be a lot of time, effort and stress avoided.

- you get more choice of potential suitable lenders.

- a broker can match your current financial circumstances with hundreds of finance offerings. It can have a huge influence on what you can do.

- a broker can do a health check on your current financial circumstances and suggest ways to improve your potential of getting a home loan.

- a broker can temper your expectations of what you want to do and what you can realistically achieve.

- the broker does all the paperwork and submission to the bank. You just have to provide the supporting documentation.

- your broker will monitor your application as it goes through the lender approval process. Any issues can be dealt with quickly to avoid delays.

Most people will use the financial expertise of a broker to get them on the road to their first home.

A broker does all the heavy lifting for you

Lenders use a number of standard credit criteria to evaluate your ‘credit risk' or ‘lending worthiness”. Not all lenders are the same however and each may place a different emphasis on some or all lending criteria. As a consequence, results can vary a lot between lenders and you may qualify with some lenders and not others.

In most instances, lenders will take into consideration your income, current credit commitments and likely living expenses incurred by you and/or your family and calculate its impact on any proposed new borrowing. There are over 100 lending elements to consider (See Table 1 below). That’s where a broker can help.

As well, home loans over an 80% LVR have mortgage insurance. This is an insurance taken out by the lender, paid for by the borrower to protect the lender should the borrower default and the lender is not able to recover the full amount of the outstanding loan. Currently there are two major players in the mortgage insurance market. Some of the bigger lenders and their branded subsidiaries self-insure. Because of their size they can offer their own type of loan insurance. So premiums can vary which might be important if your "loan setup costs" are eating into your savings.

The twist for first home buyers is that mortgage insurers also have their own set of criteria which adds another layer of complexity to the approval process. For example, some insurers may exclude some postcodes and property types. Hence, a First Home Buyer will have to look at other postcodes to get a loan approved.

A targeted assessment approach can quickly identify effective lending solutions before an application is made. A competent broker is up to date with the latest bank products and offers and in some cases can offer you finance that isn't available across the counter at many bank branches.

Finding out how much you can borrow, which lenders you qualify with and the finance that suits you can make all the difference in turning your dream into a reality.

Typical loan assessment criteria

There are lots of variables that influence the amount you can borrow and the type of loan you can get. Check out some of the criteria lenders consider in assessing your lending worthiness.Table 1: Lending criteria

A. Your personal profile

1. Current employment status (full-time, part-time, casual, contract)

2. Length of current employment

3. Employment history

4. Income (serviceability)

5. Fully verified income or self-certified

6. Credit profile (credit history, credit conduct)

7. Borrowing entity (individual, company or trust)

8. Family profile (no. of adults and dependent children)

9. Deposit contribution and/or savings history

B. Your assets & liabilities profile

1. The type of assets (cash, property, shares, boat, etc)

2. The location of property assets & LGA zonings

3. Total net worth, total asset debt, total expenditure

C. Loan profile

1. Loan purpose (Investment/Owner-occupied)

2. Loan size

3. Loan term

4. Loan to value ratio (LVR)

5. Interest rate

6. Interest type

7. Deposit required

8. Deposit sources

9. Serviceability ratios (capacity to repay)

10. Mortgage insurance requirements (if applicable)

D. Transaction costs

1. Finance or loan setup costs

2. Legal costs (mortgage documentation, conveyancing)

3. Government charges (stamp duty, searches)

4. Inbound costs (building & pest inspection; connection fees for utilities; relocation expenses, property maintenance or upgrades etc)

5. Exit or loan break costs

E. Is there a solution?

1. Does the finance package offered meet your objective/s & time frame

2. Is the opportunity worth it?

3. What are the potential risks?

4. What are the benefits for you?

First steps

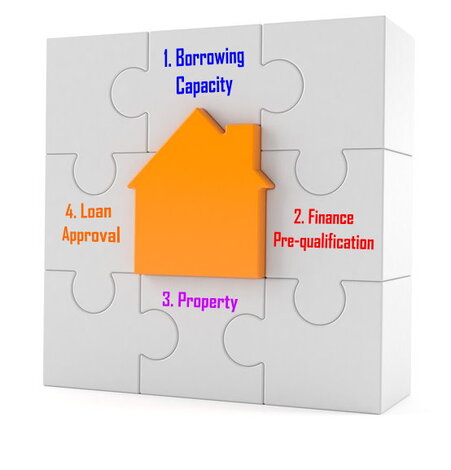

The first thing you are going to want to know is your borrowing capacity. It's like your first move on the chess board. This allows you to spend your time looking at homes that are in your price range rather than waste your time looking at homes that you ultimately cannot afford.

Lenders use a number of standard credit assessment criteria to evaluate your ‘credit risk' or ‘lending worthiness”. Not all lenders are the same however and each may place a different emphasis on some or all lending criteria (see Table 2 below). As a consequence, results can vary a lot between lenders. That’s where we can help.

firsthomebuyer.info can check your borrowing capacity with different lenders. Our targeted assessment approach can quickly identify how much you can borrow and offer effective lending solutions.

0

reviews